Few industries have proven immune to digital disruption. Even the banking industry, filled with companies that have tens and even hundreds of billions of dollars in assets and hundred-plus year histories, is finding itself under siege from startups that aim to take their place.

These so-called “challenger banks”, while nowhere near as big, powerful and rich as their entrenched competition, are finding success by revolutionizing the banking customer experience.

Here are some of the ways they’re doing it.

Rethinking what “banking” is

Different types of customers want and need different things from their bank and this gives challenger banks the opportunity to rethink what “banking” is for the customers they target.

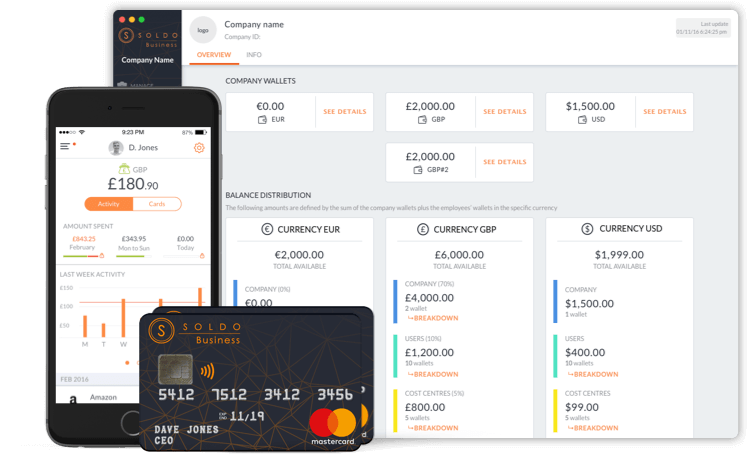

Take, for instance, UK challenger Soldo. It gives businesses the ability to deposit funds into an account held at Barclays and then issue debit MasterCards to their employees as well as contractors and departments. Through the Soldo website and mobile app, customers can track and generate detailed spending reports.

Soldo has built a host of features designed specifically for the needs of businesses that need to authorize their workers to spend. For example, limits, budgets and rules can be set for each individual card issued.

Cards can be turned on and off instantly, and overseas and online transactions can be restricted. Instant notifications can be created to ensure that the appropriate individuals or departments are alerted to transactions.

In effect, Soldo has created a bank exclusively for a very specific kind of banking customer.

Creating mobile-centric user experiences

The rise of the smartphone has changed the way individuals, particularly those under the age of 50, want to interact with their banks and challenger banks are taking advantage of this by creasing mobile-friendly user experiences.

In fact, some go so far as to make it clear that they’re all about mobile. For example, Atom’s homepage states “We’re the UK’s first bank built exclusively for mobile.”

Virtually every challenger bank offers an iOS and Android app that is designed to appeal to consumers tired of using the clunky and not-always-so-useful apps that many big banks still offer their customers.

The apps of challenger banks tend to be much slicker and, more importantly, offer functionality that makes it super easy for users to perform common functions and access the data they need.

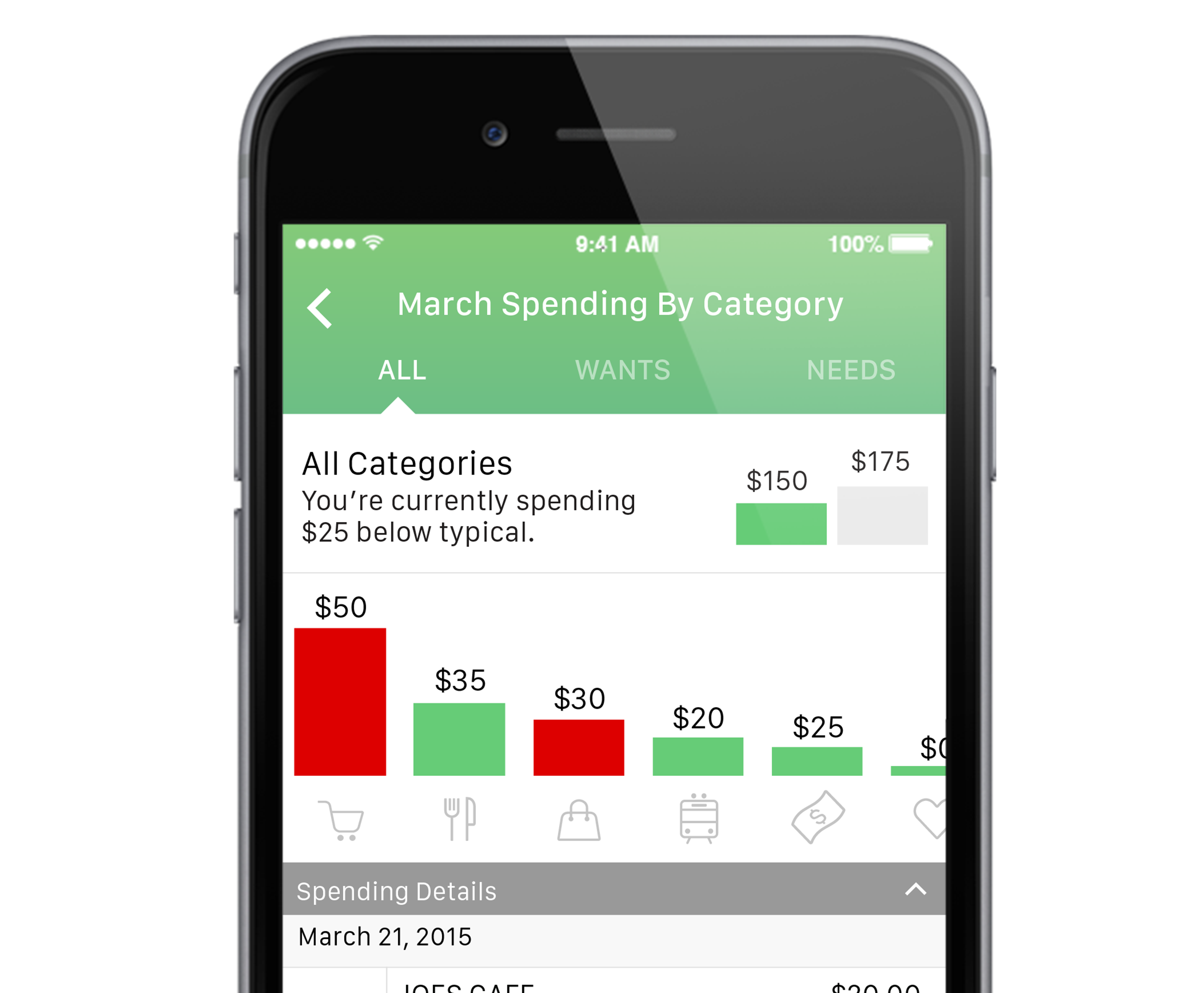

Case in point: American challenger bank Moven offers an account, debit card, and app that “all work together to help you understand and manage your spending.” When a purchase is made with the Moven debit card, the Moven app automatically categorizes the purchase and tracks spend, making it possible for Moven customers to see exactly how much they’re spending and where.

The app’s Spending Meter shows monthly spend at a glance, and a Spending Spikes feature alerts customers when Moven notices they’re spending more than usual.

Finally, Moven makes it possible for customers to send money to other people via email or SMS, even if they’re not Moven customers.

Building innovative technology

Challenger banks aren’t just putting snazzy mobile interfaces on top of old technologies. In many cases, they’re competing with big banks – most of which maintain giant legacy systems that make it more difficult for them to innovate – by building their own technology platforms from the ground up.

This technology enables them to do seemingly simple things that big banks often fail to. For example, Atom boasts that account opening and initial deposit can be performed in just minutes through a phone or tablet.

Digital, mobile-only banking start-up Monzo offers real-time balance information, noting that “it’s ridiculous that your bank still takes days to update your balance when you make a card payment”. But that’s not all. Monzo does something that most big banks would be loath to do: it offers an API that its tech-savvy customers can use to build their own banking apps.

Staying laser focused

Historically, big banks have been all things to all customers, offering checking and savings accounts, merchant accounts, personal and business loans, and so on and so forth.

But being all things to all customers is difficult, if not impossible, to do well, and startups targeting banks and other established financial institutions have taken advantage of this by focusing on specific financial services that they can build better customer experiences around. Their success has given consumers the ability to “unbundle” and select the companies they prefer for very specific financial services.

For example, a consumer might use a challenger bank like Simple to manage their money, a peer-to-peer lender like LendingClub to obtain personal loan and an alternative lender like SoFi to apply for a mortgage to buy a house.

While some challenger banks have plans to branch out as they grow, others are more than willing to partner with best of breed third parties who offer services that they don’t see as being core to their businesses. For instance, a number of challenger banks have chosen to integrate with TransferWise for international money transfers.

Offering transparent pricing

Big banks have a reputation for nickel-and-diming their customers, and scandals like those that have hit Wells Fargo have not helped banks convince consumers that they’re trustworthy.

So it’s no surprise that many challenger banking services make it a point to be transparent about how they make money. Soldo, for instance, displays all of its fees and limits prominently at signup.

What about the fine print? Simple makes fun of that on its homepage.

Adopting more efficient business models

In an effort to cut costs and eliminate increasingly underutilized physical locations, many big banks are reducing the number of branches they operate. It’s a significant undertaking that challenger banks don’t have to occupy themselves with.

That’s because virtually every challenger bank is branchless, giving these startups the ability to adopt business models that big banks, with their thousands of branches, still can’t.

In many cases, challenger banks boast that the savings they realize by not operating branches are being passed on to customers in the form of lower fees (or no fees) and higher interest rates on savings.