Access to data is the key to China's programmatic sector

Experts predict that in 2016, access to data will become more readily available to advertisers in China, which will result in the overall refinement of programmatic strategies.

Experts predict that in 2016, access to data will become more readily available to advertisers in China, which will result in the overall refinement of programmatic strategies.

Experts predict that in 2016, access to data will become more readily available to advertisers in China, which will result in the overall refinement of programmatic strategies.

I personally characterize 2015 as the year of market hype for the programmatic sector in China, because of the significant amount of programmatic growth the country experienced last year. This growth was largely driven by big brand advertisers allocating small percentages of their budgets to programmatic trials.While many brands jumped on the bandwagon purely due to this market hype, following this trend ultimately resulted in increased awareness about the different issues related to programmatic, including inventory quality, media arbitrage, and brand safety. So as this perception of programmatic continues to mature and evolve, I predict that advertisers, agencies, and brands will better understand how to create and execute effective strategies for this market in 2016.

With this context in mind, it’s worth noting that China’s programmatic market is expected to grow from 15 percent of the total display market to almost 30 percent by 2017, according to iResearch’s 2014 China DSP Industry Report.

Here are four reasons why programmatic in China will experience such rapid growth, as we head into 2016:

As I addressed in my last column, the big worry for many advertisers around programmatic lies with real-time bidding (RTB) inventory. RTB tends to consist of more long-tail inventory, which is ad inventory from lesser known publishing sources. This carries a higher risk of brand safety and viewability issues.

In addition to media quality challenges, there’s also the issue of pricing transparency. Most demand side platforms (DSP) in China have evolved from traditional ad networks, which means that they include mark-ups on top of platform fees. This middleman arbitrage hurts both publishers and advertisers.

Overall, these issues with RTB create a general lack of trust between advertisers and DSPs. Therefore, big advertisers will start to shift towards programmatic direct buying (PDB) in order to maintain direct relationships with publishers.

The PDB model operates on a fixed pass-back basis. Agencies and advertisers negotiate a fixed pass-back ratio with the publisher, and then use a third-party buying platform to pick out the impressions they want, while returning the rest.

PDB models of programmatic trading give advertisers the highest amount of transparency and control. I predict that we’ll begin to see a lot more brands shifting their programmatic strategies in this way.

Data is one of the most important elements in programmatic targeting, but the local market is generally lacking in third-party DMP providers. The most valuable data remains in the hands of the local publishers and not the DSPs.

As more advertisers realize this fact, they will not be satisfied with using second-party DMPs from the DSPs. Advertisers will demand more reliable data sources from China’s three biggest publishers – Baidu, Alibaba and Tencent (BAT), as well as other prominent Chinese vertical publishers – in response.

Both Tencent and Baidu opened up access to their third-party DMP last year, but this was mainly limited to very large advertisers with major negotiating power. Hence, the walled garden approach of bundling inventory and data is slowly coming to an end, with only Alibaba’s Alimama still operating on a closed ecosystem.

Vertical publishers that began trialing their DMP products in 2015 with selected advertisers, such as Babytree and Bitauto, are now perfecting their tagging structures. This trend will continue to rise as more publishers plan their DMP monetization strategies.

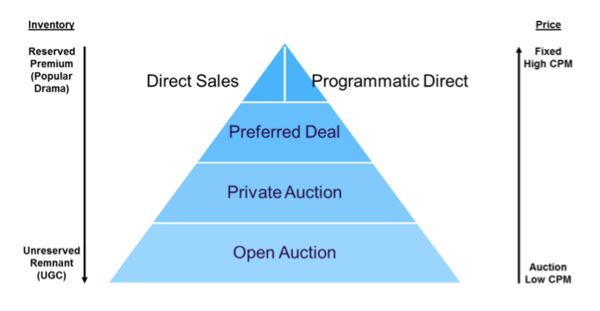

Before the emergence of PDB, publishers merely had two tiers of inventory: reserved and remnant. Reserved inventory was sold through direct sales, and remnant inventory was released on publishers’ private exchanges. During most of 2015, major publishers forbid brand advertisers from buying on their ad exchanges, which was largely done to reduce channel conflict. For example, an advertiser considered as a direct key account was not able to buy remnant at a cheaper price.

In 2016, advertisers will grow their investments in biddable inventory. With the rising advertiser demand for premium programmatic, many publishers will be forced to reassess their inventory “waterfall philosophy.” I predict that the increase in pressure to drive fill rates will cause publishers to loosen up some of their restrictions and slowly begin to open up biddable formats for key accounts.

Therefore, the rise of different trading models will require a more systematic approach in waterfall management. We will start to see more publishers clearly defining types of inventory at each waterfall level.

One of the major pain points for programmatic is measurement, especially against behavioral tags used by publisher DMPs. Currently traditional ad verification can only measure consumer demographics based on offline panels. Companies like Miaozhen Systems and AdMaster have used this methodology to roughly calculate advertisers’ target audience percentages.

However, advertisers are not content with using only demographic data. For instance, there is currently no way to verify the accuracy of Baidu’s data after an advertiser uses Baidu’s search behavioral data to place targeted ads.

A new breed of third-party verification companies that measure behavioral datasets are now emerging in response to this problem. Companies like Nielsen are partnering with Tencent for its digital ad rating (DAR) product, which uses Tencent’s behavioral data in conjunction with traditional panels to measure ad effectiveness. More companies are expected to follow suit in order to meet the growing needs of various DMP application scenarios.

This year will certainly be an interesting one for programmatic. Because BAT monopolies, DSP one-stop shops, and traditional ad networks rely on arbitrage revenue models, the market will have its fair share of challenges. However, China’s programmatic ecosystem still has a promising future ahead, as data becomes more open, premium inventory increases, and advertisers become more agile and knowledgeable.

How will these things ultimately play out? Only time will tell.

Homepage image via Flickr.

Leave a Reply

You must be logged in to post a comment.