China's real-time bidding for video programmatic is a myth

Conflicts of interests mean there is nothing 'real' about real-time bidding for programmatic video buying in China.

Conflicts of interests mean there is nothing 'real' about real-time bidding for programmatic video buying in China.

Conflicts of interest mean there is nothing ‘real’ about real-time bidding for programmatic video buying in China.

One of my clients recently asked me a very interesting question relating to a programmatic video campaign. How can a demand-side platform (DSP) guarantee a fixed cost per thousand (CPM) when buying from real-time bidding (RTB) inventory?

If the pricing is truly variable, then how can a fixed impression volume within a set campaign period also be guaranteed?

The short answer is: “This is NOT RTB buying!” The long answer is: I’ll elaborate on this in the following paragraphs.

The whole premise of ads bought via RTB is that the price is variable. However, this way of trading impacts on two other dimensions of an RTB campaign – impression volume and campaign duration.

These three dimensions are closely interlinked to one another, but one thing is certain, you can never guarantee all three at the same time in an RTB campaign.

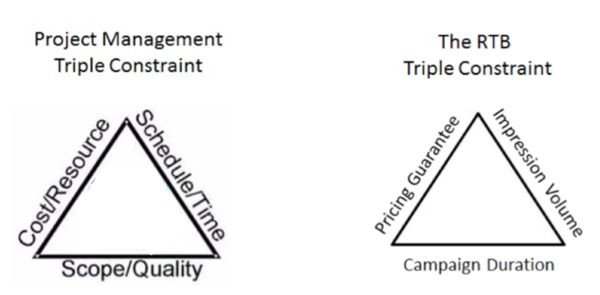

For folks familiar with the project management triple constraint concept, I’d like to draw a comparison below:

The three dimensions of the triple constraint are: scope, time and cost. The concept is that if you change one of the dimensions, the others are bound to also change.

For example, if all a sudden a project’s scope increases, additional costs are bound to arise, and the schedule will be delayed.

The same concept applies in the three dimensions that I mentioned above with an RTB campaign, which in this case I will call the RTB Triple Constraint.

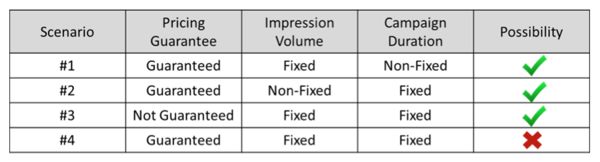

Here’s how these constraints play out in a campaign scenario:

In example one, if a DSP commits to a guaranteed CPM buying of RTB inventory while also committing to a set impressions volume, the campaign duration cannot be guaranteed.

In this case, the average CPM can be controlled via the bidding algorithm, but the catch is if there’s competition, the DSP cannot guarantee it will win the bid. Hence if it also commits to a fixed impression volume, the only way is to indefinitely delay the campaign ending time to only buy impressions that fall within the guaranteed CPM.

In the second example, if a DSP commits to a guaranteed CPM during a set campaign period, it can’t also commit to a fixed impression volume. This is because the CPM is controlled via the bidding algorithm.

If the campaign is set to end on a specific date, then there is the risk of not being able to hit the impression goal if increased competition outbids the guaranteed CPM.

In the third example, if the DSP commits to a guaranteed impression volume within a specific campaign period, it is not possible to fix the CPM.

This is because in order to hit the impression goal within a set amount of time, the CPM may have to be raised to win the bid.

While the above three scenarios are possible, the fourth and final scenario in essence, is impossible to guarantee. One of the three constraints has to be variable/non-fixed within an RTB campaign, otherwise it is simply impossible to execute.

The triple constraint is applicable to all RTB formats. For example, in SEM we would never expect a fixed cost per click (CPC) and a set number of clicks all within a specific time.

Most of the time, for an always-on campaign, we will set an upper limit on CPC. In that way, the amount of clicks can’t be guaranteed.

The other option is to set the total number of clicks to what we’d like to have within a set campaign period, meaning the CPC would then be variable.

So, if it’s impossible to guarantee the CPM, volume, and duration, how are local DSPs in China doing it? The truth is that in the video space, true RTB is not all that common.

Even though video publishers all have private exchanges, most DSPs are buying (some in advance) through preferred deals using a fixed price, then packaging their services and inventory as RTB to sell to advertisers.

This allows the DSP to have a fixed procurement cost, further enabling them to make a consistent mark-up/margin on top.

Since the DSP’s CPM procurement is fixed (and sometimes significantly lower than the price given to the advertisers), the three dimensions – under the guise of RTB inventory – can be guaranteed. In the end, it comes down to how much mark-up the DSPs are willing to sacrifice in order to hit the advertiser’s various KPI’s.

I wholeheartedly believe that this model of “fake RTB” is ultimately detrimental to the development of the programmatic industry in China. The lack of transparency is affecting all relevant players up and down the ecosystem.

This is what I believe should happen for this change:

Advertisers who want to truly invest in programmatic video inventory have two options.

The first is to cut the DSP out completely in their ability to influence media allocation by negotiating preferred deals directly with the publishers. They then pay the publishers directly based on the amount of impressions bought, and only allow the DSP to charge an optimization or technology fee.

The second option is to go around the DSP and negotiate directly with the exchanges, this will truly be a floating CPM bought via RTB. Again, in this way the DSP should only be allowed to charge a tech fee. This is the true from of how a “pure” DSP arrangement should work.

Currently, publishers sometimes make even less revenue than the DSPs due to the high mark-ups. They tolerate this because the DSPs help them to increase their inventory fill rates.

This imbalance occurs when big advertisers target premium channels in China’s affluent tier-one cities, leading to a major imbalance in lower tier inventory fill rates. This is where the DSPs help the advertisers correct the imbalance by filling the lower-tier inventory.

However, by continuing to give-in to the DSP preferred deal volume commitment, publishers’ remnant inventory never gains significant bidding competition. Publishers should take a leap of faith by reducing the percentage of inventory sold via fixed price commitments.

I firmly believe that RTB should be the most expensive type of inventory sold, and once the DSPs are forced to bid against each other, then overall inventory value can be increased.

In the old days, agencies used to give a percentage of their budget to the ad network so they didn’t have to deal with dozens of smaller publishers. This way of working didn’t change when the networks evolved into DSPs locally.

Now, as programmatic has grown to be a significant part of advertiser digital spends, the DSPs have been left to directly manage a large portion of the advertiser’s investment. The risk here is that the agencies are essentially cultivating their own demise: the DSPs.

The “P” in DSP stands for platform, a platform company is supposed to focus on their product, not by influencing the selection and allocation of media – that’s the job of the agencies!

If the agencies don’t wake up to this fact, their procurement power will flow slowly from their own hands to the DSPs. Hence, they should take the media allocation and procurement power back from the DSPs, negotiate their own rates from either the publishers or the exchanges, and force the DSPs back into a tech fee model.

Leave a Reply

You must be logged in to post a comment.