How financial services CMOs should approach regulation

Following the global financial crisis of 2008, which many blamed on rampant greed and fraud in the financial services sector, regulators around the world rushed to implement new rules that would prevent another crisis.

Many of these rules were focused on consumer protections designed to reduce the risk that consumers would fall victim to unscrupulous banks and lenders. For example, in 2014, the E.U. adopted the Mortgage Credit Directive, a regulation package that covers all consumer mortgage lending. Member states of the E.U. were required to implement the regulations in their national laws in 2016.

In the U.S., in 2010, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act, commonly referred to as Dodd-Frank, which established a new government agency, the Consumer Financial Protection Bureau (CFPB), that has broad oversight and rule-making powers.

Since 2012, the CFPB has issued rules on a wide range of matters including mortgage issuance and servicing, auto loans, debt collection, credit reporting and consumer disclosures. The CPFB is also increasingly weighing in on issues that are coming to the forefront of the financial services industry as fintech innovation creates new opportunities for established firms and upstarts alike.

For instance, the fintech revolution is highly dependent on the ability of financial services providers to access consumer financial data, which has not surprisingly been a source of friction between established firms like big banks, which have lots of customer data, and startups, which want access to data.

In an effort to begin addressing this, the CPFB has issued consumer protection principles for consumer-authorized financial data sharing and aggregation. These are similar in nature to the Open Banking reforms initiated by the Competition and Markets Authority’s (CMA) in the U.K.

With the growing number of rules, proposed rules and principles being promulgated by regulatory bodies in key markets around the world, it’s becoming increasingly difficult for financial services CMOs to keep up.

So how can they ensure that their companies’ marketing activities and sales practices are above board?

Fortunately, there is a reasonably good solution to this: in balancing what’s permitted by law and what consumers feel is fair, CMOs would be wise to apply the Golden Rule to how they market and sell their products and services. In other words, at all levels of the customer lifecycle, financial services companies should treat customers and potential customers the way the people running them would want to be treated themselves.

While seemingly a no-brainer, such an approach can be challenging because it will often require firms to rethink their products and services, and their business models. To do that successfully, CMOs need to make sure they are involved in broad strategy decisions and ensure that those decisions take into account what is most likely to resonate with customers.

Looking at banks, for example, it’s no secret that customers hate hidden fees. Overdraft charges, in particular, are extremely unpopular, in part because they have too often been employed in a fashion seen as predatory.

The conundrum banks face is that if they reduce (or eliminate) the revenue generated by overdraft charges and the like, it makes it more difficult for them to offer services, like no-fee checking, that customers have become accustomed to.

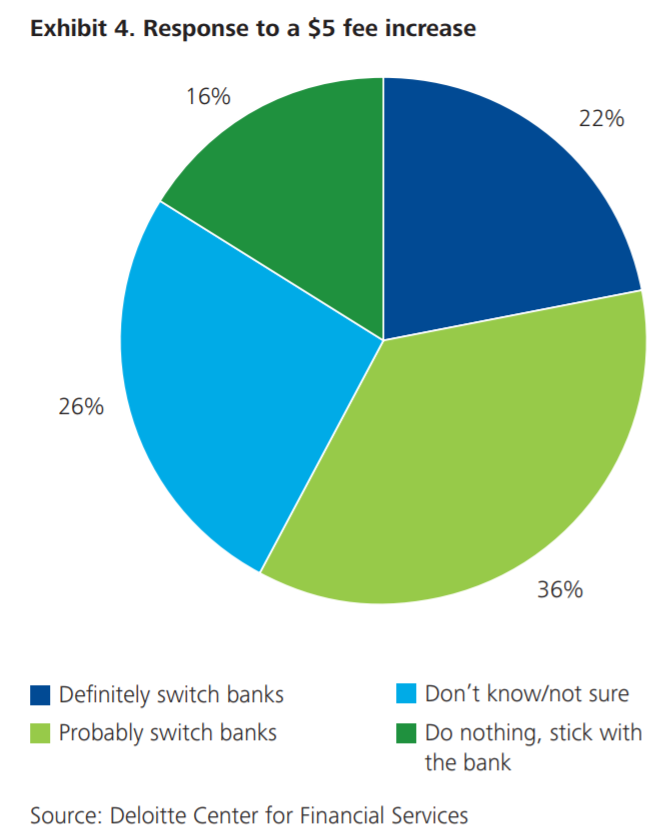

Going from free to fee is not easy. Research by global consultancy Deloitte found that “nearly six in ten [banking customers] said they would probably or definitely switch if their primary bank charged an additional $5 per month for the same level of services.”

But Deloitte also found that there were a lot of areas where banks were falling short, hampering their ability to make necessary changes to their products, services, and business models.

Specifically, Deloitte suggested that “understanding the unique characteristics and preferences of an institution’s customers may be essential to ensuring new fees do not harm the primary customer base or derail an institution’s business strategy”, adding that “in many cases simple demographic or satisfaction analysis is probably insufficient for segmentation and pricing strategies; successful implementation of changes to pricing models will likely rely on a more complete understanding of differences in customer preferences.”

Deloitte also found that banks haven’t done the best job at communicating to their customers the value of their products and services despite the fact that, interestingly, consumers are more receptive to such messaging from banks than they are to such communication from airlines and telecoms.

At the end of the day, as financial services CMOs grapple with these issues, it’s important for them to take a customer-centric approach, not a regulation-centric approach. In other words, engagement with customers should be driven by the best interests of customers, not by a desire to go as far as the rules permit.

Leave a Reply

You must be logged in to post a comment.