What can we learn from the successes and failures of Unicorns?

The term “unicorn” is commonly used to define a privately-owned company that is valued at $1 billion or more. Although named after a mythical creature, they have been appearing with increasing regularity and they provide lessons for businesses of all sizes.

Since the label was first used in 2013 by venture capitalist Aileen Lee to describe start-ups that reach the lofty heights of a $1 billion valuation, “unicorn” has come to signify new and disruptive businesses that capture the imaginations of consumers and investors alike.

The name is derived from the fact that finding such companies was considered about as likely as finding a unicorn, statistically speaking. Historically, the idea of a start-up reaching such a stratospheric valuation had indeed been the reserve of a very select few. Not quite as rare as finding a unicorn, but very rare nonetheless.

That is far from the case nowadays, with 217 companies meeting the unicorn criteria at the latest count, including the likes of Spotify, Uber, and Pinterest. The visualization below shows the increasingly crowded nature of this exalted space, as more and more start-ups have experienced phenomenal growth in their valuations:

Tellingly, these companies stay private for much longer than their relative equivalents did just a few decades ago. A large technology company takes 11 years to go public nowadays, compared with an average of four years as recently as 1999.

The availability of VC funding has shifted this dynamic altogether, as fast-growing start-ups can access capital to fuel their growth plans without offering their shares to the public market.

When the Initial Public Offering (IPO) finally does arrive, it is a newsworthy spectacle that draws attention from far and wide. The media frenzies that accompanied the respective IPOs of Facebook and Snap certainly attest to this.

Unicorns are now a global phenomenon, however.

Although the majority of unicorns start their life in Silicon Valley, there are many success stories in Asia, Europe, Africa and South America.

Moreover, they span an impressive array of industries, from VR to Big Data and Healthcare.

We can see that there is significant variety within the list of unicorn companies, in terms of their geographical distribution, their product offering, and the industries in which they operate.

Beyond these differences, however, there are some common threads that unite these companies. They all solve problems in novel ways, using technology to create platforms that can create exponential growth. That combination gets investors excited, for understandable reasons, but when everyone is on the lookout for the latest unicorn, chances are they are going to find it. There are, therefore, pitfalls as well as opportunities.

Undoubtedly, there is much to be learned for any business from these hugely successful start-ups. Below, we take a look at the core lessons to be drawn from the successes and failures of unicorns.

Consumer journeys are increasingly fragmented, with a huge amount of choice and few incentives for blind loyalty to a brand. The onus is on companies to stand out from the crowd and attract repeat custom.

Companies that do end up earning the unicorn honorific begin with a simple premise. They observe challenges that people face everyday and they devise innovative solutions that offer real value to consumers.

As technology changes our behaviors and the expression of our demands, new opportunities to achieve this arise constantly.

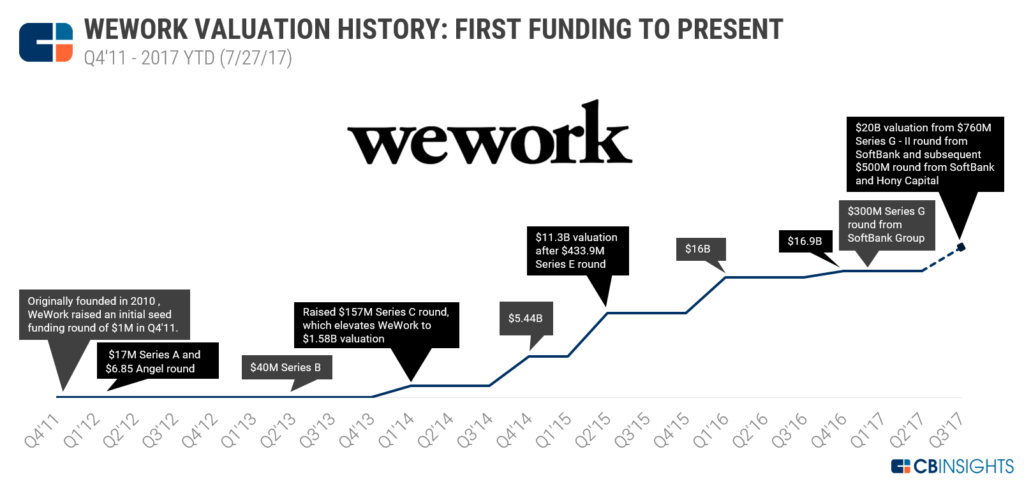

WeWork, valued at $20 billion, offers affordable office space to start-ups. The key to its success, however, has been in understanding the desire among younger workers for communal, social spaces to network with other fledgling businesses. There have been reports of the WeWork CEO encouraging his staff to populate these communal areas when investors visit (“Activate the space”, the slogan goes), to drive home the sense that the company is about community rather than just transactions.

This has been a compelling narrative for investors, who see it as a modern take on the traditionally stuffy world of office space rental. Although they claim to spend very little on advertising, WeWork has still become one of the most valuable unicorns in the US by tapping into the zeitgeist.

We see this same story played out across a number of unicorn businesses. They use technology to create seamless interactions between consumers and products or services, inculcating a sense of community in the process.

No amount of marketing or commercial nous will attract investors or increasingly savvy consumers. These elements can facilitate a solution, but they cannot stand in its place.

To aim to simply become a “unicorn” business is to put the cart firmly before the (behorned) horse. Study the available technology to identify ways you can solve real-world problems for people, then the rest will follow.

Unicorns achieve huge valuations based on their projected future earnings, rather than their historical performance. That stands to reason; start-ups have little in the way of historical performance, after all.

The reason investors have such unprecedented confidence in their ability to grow is that they are built using a platform business model. A platform provides an arena for exchanges between different parties and can be contrasted with the traditional pipeline business model.

Where pipeline businesses tend to stagnate as their costs grow in line with income, platforms deliver exponential growth. There are plentiful examples of successful platforms in the 21st century, including current unicorns such as Airbnb and Uber. Although these companies of course incur increasing variable costs as they grow, these are minimal when compared to a traditional business like an automotive manufacturer.

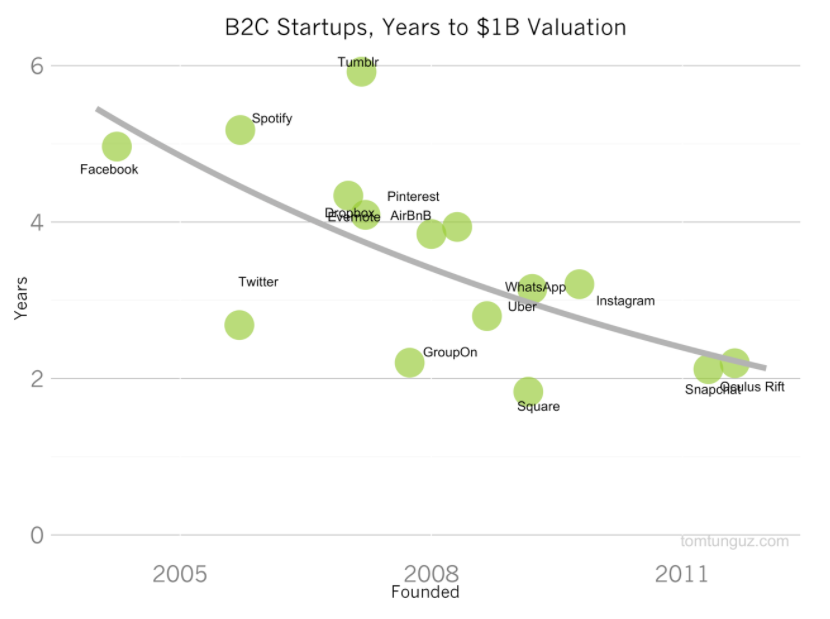

This helps explain why the length of time required to reach a $1 billion valuation for a start-up is decreasing significantly.

Tom Tungutz, a venture capitalist, used a logarithmic regression model to show the number of years it has taken companies to reach the $1 billion mark since their founding.

The acceleration is very marked and it points to a number of potential driving forces. It also poses the question of just how sustainable – and in fact, just how real – this new landscape is. These 217 companies have a cumulative value of $752 billion, after all.

The trend is more dramatic still when we isolate the B2C unicorns from their B2B counterparts:

These tech companies are inherently driven by a belief on the platform business model to create huge growth over long periods of time. The trend is so recent that we do not yet have access to reliable data with which to assess the accuracy of these predictions. However, we do know that early adopters such as Apple, whose App Store is an archetypal platform business born in 2002, has been a continuing success.

Research conducted by the UBC Sauder School of Business and Stanford University found that 49% of “unicorns” are not actually worthy of the title. Their analysis sought to quantify the fair value of these companies, rather than their value as defined by investors. In fact, they found that 11% of “unicorns” are over-valued by more than 100%.

It is worth quoting directly from this research to highlight why exactly this overvaluation occurs:

Current valuations make a misleading assumption: that a company’s shares have the same price as the most recently issued shares. This oversimplification significantly inflates valuations, since the most recently-issued shares almost always include perks not found in previously-issued shares. Specifically, we found that 53 per cent of unicorns gave their most recent investors either a return guarantees in IPO (14 per cent), the ability to block IPOs that did not return most of their investment (20 per cent), seniority over all other investors (31 per cent), or other important terms.

The rate of growth in The Unicorn Club is slowing, too. 19 new members were admitted in 2016, the same number as in 2014. As rational beings, we can understand this. However, we are often not quite so rational and investors want to see endless growth.

We should be accustomed to cycles of boom and bust by now, but hype can be very seductive. There have been some genuinely huge success stories in the tech space from which many have profited, so it is to be expected that we are on the hunt for the next unicorn. That hope can blind us to the cold, hard facts, however.

The Sauder School of Business sounded an important note of caution to employees at unicorn companies, too:

Our findings also have implications for the rank and file employees of VC-backed companies, who often receive much of their pay as stock options. Our analysis finds that these employees are receiving much less than they think they are in fair-value.

As a result, we can learn from this research that companies should stay focused on improving their offering and preparing to fend off new competitors. Valuations can very quickly go up, but they are very fragile things that are driven mainly by emotion.

The bigger they are, the harder they fall.

It was always predictable that companies that become so wealthy, so quickly, would meet some challenges along the way.

What we may not have expected, however, was that they would attract quite so much controversy.

Uber has endured what we could diplomatically call a difficult year. The Guardian has written a lengthy list of Uber’s PR disasters over the past few years, but these are not incidents that are isolated to the ride-sharing giant.

WeWork has been drawn into an unsavory lawsuit with its cleaners, who claim they are underpaid and poorly treated by their employers. Airbnb has made some very powerful enemies in the hospitality space, too.

Facebook has been a victim of its own success, we could say, with investigations ongoing into its role in the 2016 US elections. It is Facebook’s stance as an impartial platform that is under scrutiny, as this has allegedly allowed foreign agents to promote their agenda on the social network. There is a delicate balance to be struck here between a free market that allows companies to flourish and interventionist policies that protect the public and encourage competition.

In essence, although we are dealing with tech-focused companies, we shouldn’t forget that people still dictate the fate of a business.

These are new problems caused by familiar sources. Companies should remember, as they grow, that there is still a core need to act in the best interests of their employees and their customers. Even the most sophisticated, automated technology depends on people both for its creation and for its successful adoption. It seems many unicorns are learning these lessons the hard way. For all their successes, we can still learn just as much from unicorns through their transgressions.

Leave a Reply

You must be logged in to post a comment.